Bitcoin is getting into an period the place macro order is extra vital than narrative.

Inventory markets are buying and selling close to report valuations, actual yields stay excessive, and credit score markets have expanded into an more and more opaque a part of the monetary system. None of those phrases assure any impending interruption. However collectively they type a backdrop that may be a window of excessive volatility for danger property.

Within the case of Bitcoin, key questions heart on whether or not stress will emerge within the monetary plumbing beneath rising asset valuations, and the way shortly policymakers will act to comprise the stress.

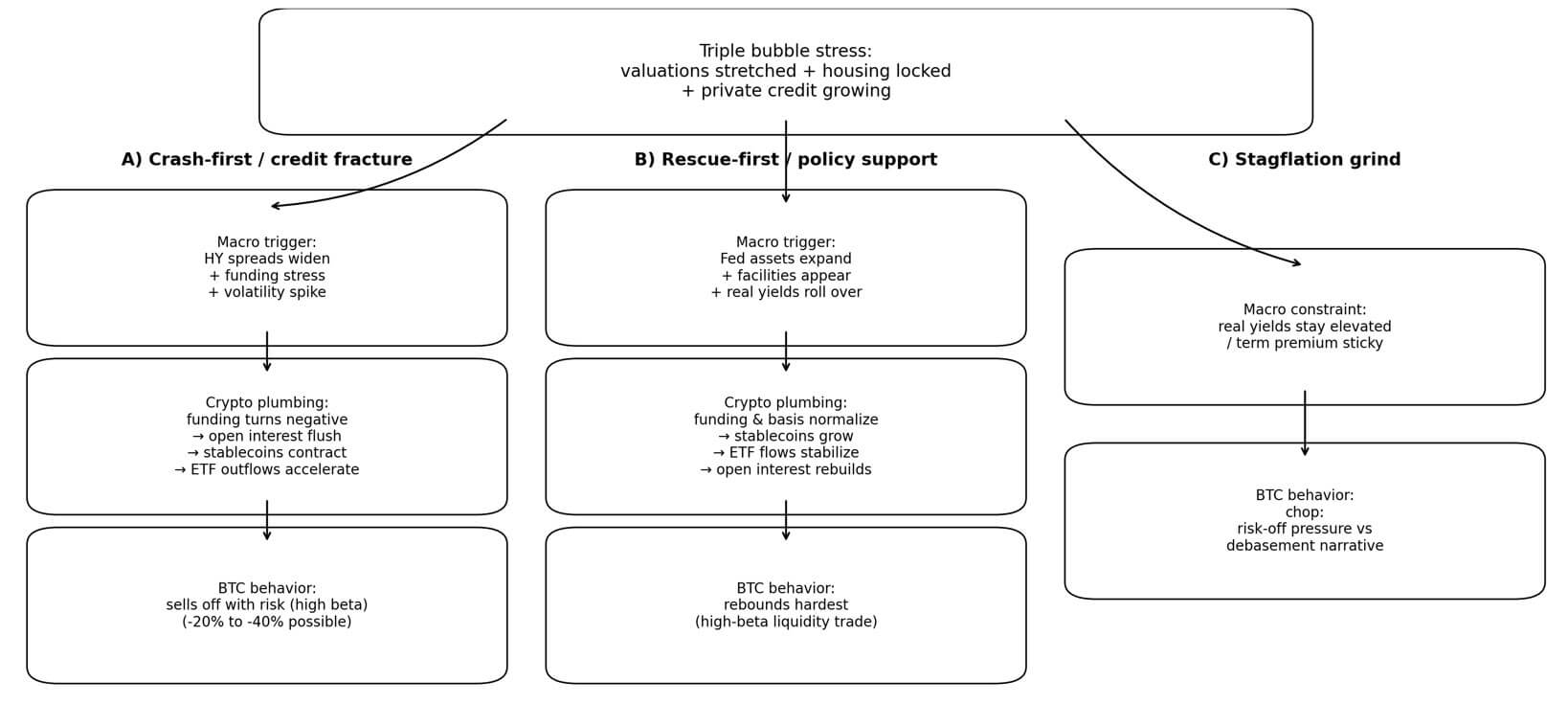

Macro strategist Michael Pent describes the present state of affairs as a “triple bubble.” Inventory costs are at near-historic extremes, housing is constrained by mortgage rates of interest shut to six%, and the personal sector is competing for credit score with the intention of reaching $2 trillion in property beneath administration. Though labels are provocative, this framework is helpful as a result of it emphasizes ordering.

If belief collapses first, liquidity might evaporate and Bitcoin may very well be bought off together with every little thing else. If coverage assist is obtained earlier than the rift widens, Bitcoin might as an alternative behave as a high-beta liquidity commerce and rebound sooner than conventional danger property.

Programs not often break as a result of valuations seem extreme. Credit score and bond plumbing collapses when pressured to promote, and Bitcoin’s 24/7 liquidity means each panic and bailouts are more durable to commerce than most.

Latest knowledge point out that stress alerts are nonetheless accumulating with out fractures occurring.

Adjusted spreads for ICE BofA US excessive yield choices hit 2.95% on February 23, nonetheless tight in comparison with the disaster regime.

The Federal Reserve’s steadiness sheet was $6.613 trillion as of February 18, a rise of about $28.8 billion in 4 weeks, however this can be a gradual enlargement that doesn’t point out emergency liquidity.

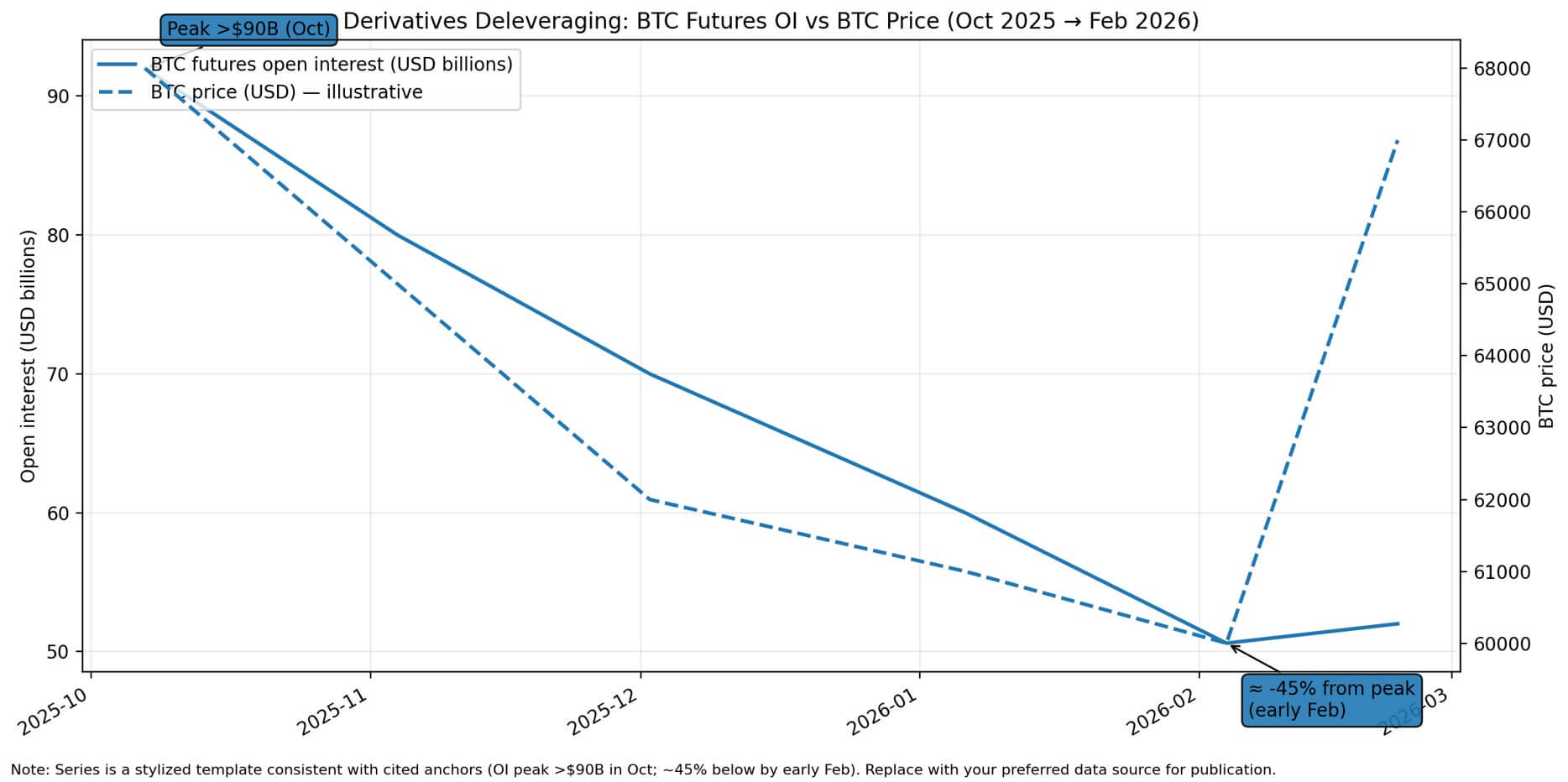

Actual yields, as measured by 10-year TIPS yields, hovered round 1.80% as of February 20, rising sufficient to place stress on non-yielding property. The stablecoin market capitalization remained at roughly $308.8 billion, with a 30-day change of -0.18%.

The Spot Bitcoin ETF has recorded a complete of about $2.6 billion in outflows for the reason that starting of 2026, with about $4.3 billion misplaced in 5 weeks.

Bitcoin bought first, questions requested later

Deflationary liquidation begins within the credit score market, not in inventory indexes.

Excessive-yield spreads widen quickly, funding markets present stress, volatility spikes, and the one place anybody needs is money.

Bitcoin actions throughout these home windows are predictable. Everlasting funding charges flip destructive, open curiosity is dumped as leverage positions are unwound, stablecoin provide is contracted as liquidity leaves the system, and ETF outflows speed up.

March 2020 gives a clear historic anchor. On March 12, amid a worldwide liquidity shock, Bitcoin plummeted by practically 40%, promoting off together with shares, credit, and commodities as individuals scrambled for greenback liquidity.

Credit score-driven liquidations can simply trigger Bitcoin to fluctuate by -20% to -40% inside a number of days.

Van Eck famous in early February 2026 that open curiosity in Bitcoin futures peaked in October at over $90 billion, and the market has since decreased greater than 45% of its peak leverage, leaving room for additional pressured promoting if credit score stress materializes.

Moody’s expects personal credit score property beneath administration to exceed $2 trillion in 2026 and strategy $4 trillion by 2030, and Reuters stories that Financial institution of America has dedicated $25 billion to the sector.

This development concentrates credit score danger in opaque constructions with lengthy lock-ups and weak covenant safety.

If a credit score occasion triggers a pressured asset sale of a personal credit score portfolio, the ripples will have an effect on the general public market via collateral calls and margin pressures. And because the most liquid danger asset 24/7, Bitcoin absorbs a disproportionate quantity of promoting.

Bitcoin on the forefront of coverage response

The reverse sequence begins with seen coverage assist.

The Fed’s steadiness sheet will broaden, emergency services will come into play, and actual yields will fall. Bitcoin’s response in these regimes is equally predictable. Funding and foundation normalize, stablecoin provide will increase as liquidity returns, ETF flows stabilize or flip constructive, and open curiosity rebuilds.

In a tangible rescue regime, Bitcoin usually behaves like a high-beta liquidity commerce, with no credit score danger and no disappointing returns, and recovers sooner than conventional danger property. This acts as a liquid declare in opposition to a set provide monetary asset that advantages when actual yields decline.

The March 2023 banking disruption gives that template. Bitcoin rose 26% in a single week and practically 40% in 10 days as financial institution stress modified expectations for coverage easing and ushered in eventual liquidity assist from the Fed.

In February 2026, Bitcoin soared from about $60,000 to greater than $70,000 in a single day, its largest single-day acquire since March 2023, highlighting how macro danger sentiment stays a dominant issue throughout stress home windows.

Bitcoin crashed together with every little thing else in March 2020, on the identical time the Fed reduce rates of interest to zero, started limitless quantitative easing, and established an emergency lending facility inside weeks.

As actual yields remained sharply destructive and authorities spending soared, Bitcoin recovered from its March 12 lows and quintupled over the following yr.

The lesson is that Bitcoin trades liquidity cycles with a better beta than most different property, and timing is extra vital than narrative.

If neither path is dominant

Probably the most troubling state of affairs is one by which inflation stays persistent, bond markets demand larger time period premiums, and actual yields stay excessive, limiting policymakers’ skill to offer fast reduction with out reigniting inflation issues.

On this regime, Bitcoin is chopped. Danger-off pressures compete with degrading hedging narratives. If actual yields turn into robust or coverage assist disappoints, the bull market subsides.

The ten-year TIPS yield of 1.80% is effectively above the zero-to-negative actual yields that characterised Bitcoin’s strongest interval.

Freddie Mac’s 30-year fastened mortgage rate of interest averaged 6.01% as of February nineteenth.

In keeping with Advisor Views, the Buffett index is round 206%, the very best stage in sequence historical past, suggesting there’s little room for a number of expansions in inventory valuations absent earnings development or a decline in low cost charges.

If credit score stress arrives with no swift coverage shift, Bitcoin will face a regime with no dominant path to liquidation or rescue.

Monitoring migration

A easy framework for monitoring which regimes are energetic combines 4 inputs which can be up to date weekly. That’s, the change in Fed whole property over 4-8 weeks, the change in stablecoin market cap over 30 days, the change in excessive yield unfold over 2-4 weeks, and the change in 10-year actual yield over 2-4 weeks.

When the rating plummets, Bitcoin tends to commerce like a high-beta asset throughout liquidity occasions. Because the rating will increase, Bitcoin tends to outperform as reflation expectations improve.

Present readings recommend a impartial to destructive liquidity background.

The Fed’s steadiness sheet is rising slowly, however not quickly. Stablecoin provide is flat to barely lowering. Credit score spreads stay tight. Actual yields are rising and protracted. Outflows from Bitcoin spot ETFs proceed, with open curiosity in derivatives falling to almost half of its peak.

This case is much like a market awaiting a catalyst, both credit score stress that forces liquidations or coverage assist that reinvigorates liquidity buying and selling.

Inform arrives at credit score plumbing

A sensible monitoring framework focuses on credit score and cryptocurrency plumbing. The rise in high-yield spreads from tight ranges means that credit score market confidence is weakening.

Authorities bond volatility and time period premium pressures reveal whether or not bond markets are pricing coverage flexibility or constraints. The flat or declining Fed steadiness sheet regardless of widening spreads confirms the shortage of a backstop.

On the crypto facet, a pointy drop in open curiosity signifies a pressured promote. The shrinking market capitalization of stablecoins signifies that liquidity is being drained from the system. The continued outflow of ETFs confirms the institutional risk-off angle.

Affirmation of rescue comes via varied channels.

The numerous improve within the Fed’s whole property from the earlier week means that it’s actively offering liquidity. The rollover within the 10-year TIPS yield signifies that actual yields are falling. The rise in stablecoin provide in parallel with the normalization of derivatives funding helps the return of liquidity to the crypto market.

The transition from liquidation to rescue usually occurs shortly, as in March 2020 when Bitcoin collapsed and rebounded inside weeks as coverage assist materialized.

Triple bubble idea is most helpful as an ordering framework, not as a prediction.

A credit score bust forces a liquidation, throughout which Bitcoin trades for pennies in opposition to the greenback. Coverage bailouts have brought on a surge in liquidity, with Bitcoin main the way in which amongst conventional property.

The present macro setting, consisting of excessive valuations, rising actual yields, tight credit score spreads, secure stablecoin provide, and sustained ETF outflows, means that whereas the market is beneath stress, now we have not but skilled a breach within the credit score pipeline that may pressure a sell-off.

Bitcoin’s subsequent large transfer relies upon much less on whether or not a bubble exists and extra on whether or not credit score collapses earlier than the Fed bails it out.