CryptoQuant Founder and CEO Ki Young Ju declared on June 17, 2026, that the era of making money by simply issuing a token is over, marking a structural shift in the digital asset market.

Ju stated in a thread on X that while altcoins are not dead, those built solely on narratives face a much harder environment. He argued that the market has matured to a point where investors now prioritize real revenue, active users, and long-term business models over speculative hype and storytelling.

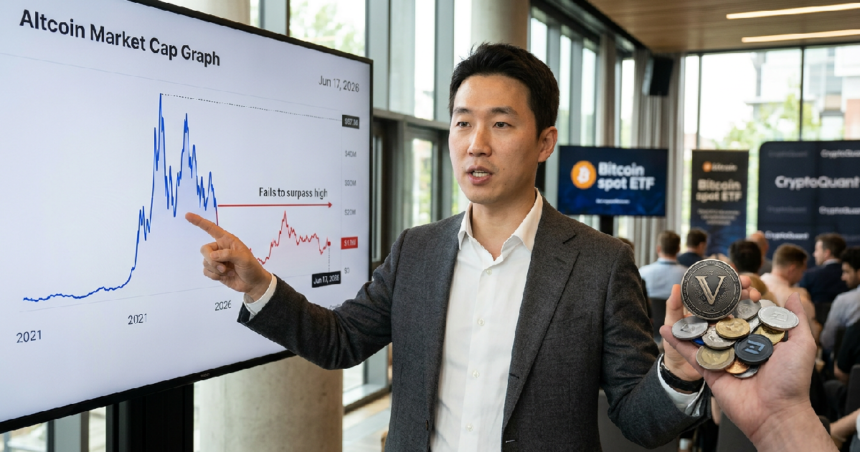

The CryptoQuant executive noted that the total altcoin market capitalization has failed to surpass its 2021 peak, even as Bitcoin attracts fresh liquidity via spot ETFs and traditional finance. Ju advised his followers that 99.9% of altcoins should be rejected, though he clarified that this does not mean every token is valueless.

He compared the current shakeout to the internet industry following the dot-com bubble, where the disappearance of weak projects paved the way for stronger businesses to emerge.

This market evolution is unfolding as mid-cap tokens face selling wave pressures, leaving many retail investors underwater. Ju acknowledged the frustration of those who have been “hurt” by altcoin volatility, noting that many have turned into “Bitcoin maxis” out of necessity.

Despite this, he urged a selective approach rather than total prejudice, claiming that some tokens remain worth holding long-term if they connect to real businesses or fit broader financial trends.

Survival categories for the post-narrative altcoin era

Ju outlined three specific categories of altcoins that he believes possess the durability to survive this shift. These are projects that move away from pure speculation and toward tangible utility and economic activity. By focusing on fundamental value, these assets distance themselves from the “trash” that Ju says comprises the vast majority of the current market.

The first category involves global internet companies that have developed tokenized market layers. These projects are tethered to large, existing businesses with strong execution and real revenue. Ju named BNB, associated with Binance, and GRAM (formerly TON), linked to Telegram, as primary examples. Because these tokens provide exposure to established ecosystems, they offer more stability than projects lacking a parent business model.

Decentralized finance (DeFi) services with real revenue represent the second category. Ju emphasized that projects with credible founders and governance structures that respect token holders will be the ones to endure. He specifically highlighted decentralized exchanges like Hyperliquid, which has gained attention in 2026 for its high perpetual futures volume and fee generation.

As the crypto utility window dictates success, real income becomes a non-negotiable metric.

Broader financial trends and blockchain infrastructure

The third group of survivors includes projects tied to larger financial shifts, such as Stablecoins and Real-World Assets (RWAs). These assets connect blockchain technology with traditional economic activity, such as tokenized stocks or government bonds. Ju also identified blockchain infrastructure for AI agents as a potential growth area, suggesting that automated agents will eventually use blockchain to transact across the internet.

These practical use cases are becoming the primary driver of value as the “narrative-only” model fails. While stories still matter in crypto, Ju warned that they can no longer carry weak projects on their own. This reflects a broader trend where capital no longer spreads evenly across the market but instead rotates between specific sectors that can demonstrate genuine economic activity.

Why the traditional Altcoin Season model is failing

The historical pattern of a rising Bitcoin price leading to a universal surge in altcoins appears to be broken. Ju pointed out that millions of tokens are now competing for a finite pool of capital, making the old “Altcoin Season” less predictable.

Instead of a broad rally, the market is seeing “narrative mini seasons” where liquidity concentrates in narrow sectors like AI tokens or memecoins before moving on.

Structural issues are also weighing down the sector. Institutional money remains concentrated in the relative safety of Bitcoin and Ethereum rather than trickling down to high-risk assets. Furthermore, significant token unlocks are pressuring prices by increasing circulating supply without a corresponding increase in demand. This has caused the altcoin market cap, when tracked against Bitcoin, to drop to its lowest level since 2022.

The risks of holding legacy tokens were underscored in June when Upbit moved to delist the NKN/BTC pair. That token remains roughly 99.5% below its all-time high, serving as a concrete example of the “dead” projects Ju described.

For investors, the takeaway from the CryptoQuant CEO is that research must now go beyond social media sentiment to analyze protocol revenue and business durability. While Ether enters rare accumulation phase territory, the same cannot be said for the vast majority of the token market.